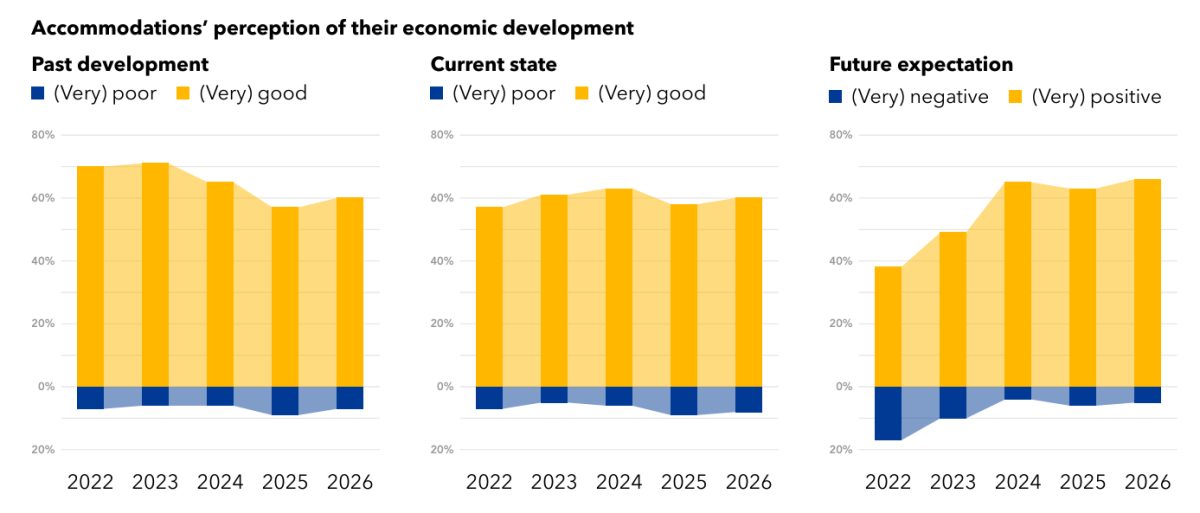

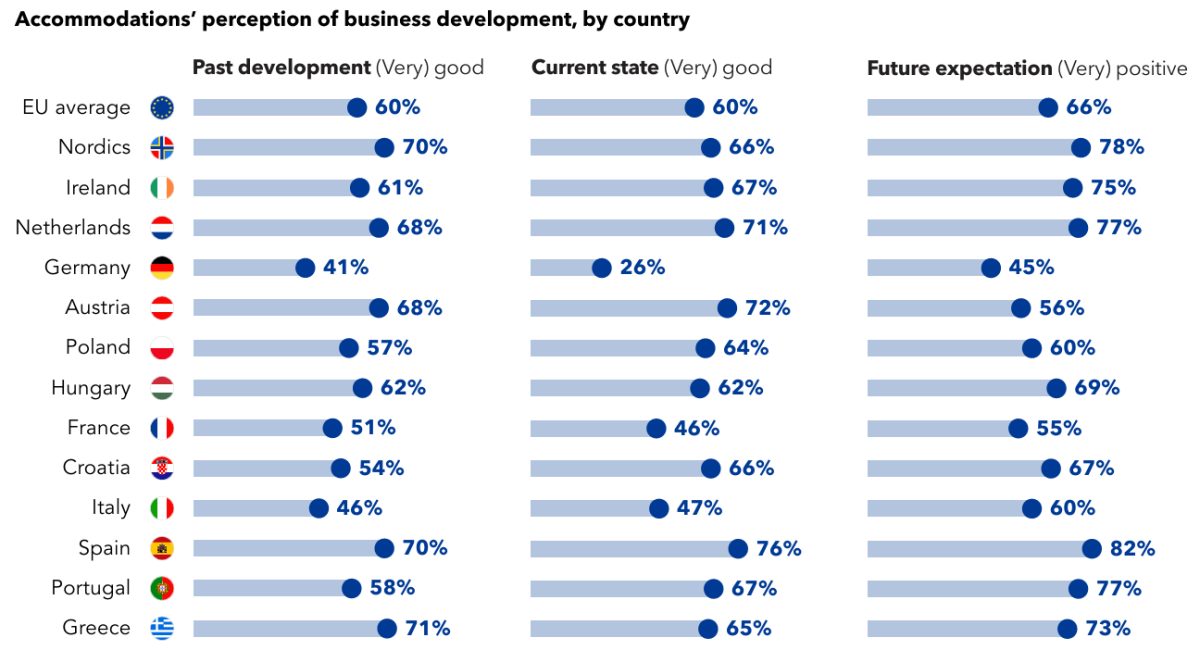

The European accommodation market is feeling optimistic again. Two-thirds of hotels and guesthouses across the continent expect solid performance over the next tourism season, and roughly 60 percent report they're in decent financial health right now. Occupancy rates are climbing, room prices are holding steady, and the worst of the pandemic's chaos seems firmly in the rearview mirror.

But scratch the surface of Booking.com's latest European Accommodation Barometer, and a more complicated story emerges. The recovery isn't evenly distributed. Large hotel chains are racing ahead while independent properties are struggling to keep up, creating a widening divide that could reshape the European lodging landscape for years to come.

The Numbers Don't Lie About Scale

The data pulled from 1,240 hospitality executives and managers across 24 European markets paints a stark picture. Around 72 percent of large hotel chains describe their financial situation as positive. For independent properties? That drops to 55 percent. When it comes to raising room rates, 47 percent of chains managed it while only 37 percent of independent operators saw similar success. Occupancy growth tells the same story: 56 percent for chains versus 46 percent for independents.

What's happening here is textbook economics. Big chains have the resources to invest in technology, marketing reach, and operational efficiency. They can negotiate better distribution deals, absorb price fluctuations, and weather downturns. Independent hoteliers and guesthouse owners? They're working with leaner budgets and smaller marketing footprints, making every booking season feel like a white-knuckle ride.

Cybersecurity Is the New Dividing Line

If financial performance is one way the gap shows itself, cybersecurity is another, and this one keeps hoteliers awake at night. The report found that 66 percent of European accommodation providers feel prepared to handle cyber threats. But dig deeper and the confidence collapses for smaller operations.

Nearly all large companies with 250-plus employees say they're well-prepared for attacks. Small properties with fewer than ten staff members? Only 60 percent feel confident. The training gap is even more alarming. While 89 percent of larger companies invest in cybersecurity training for staff, just 49 percent of small businesses do. When it comes to regular audits and external support, small properties lag significantly behind.

This matters because small business owners worry more about these threats. One-fifth of independent operators list cyberattacks as a major risk for the coming season, compared to just 9 percent at larger firms. Payment fraud concerns follow the same pattern. The irony is cruel: smaller properties get fewer attacks, likely because they're less visible targets, but they're also less equipped to detect and stop what does hit them.

Weather and Logistics Are the New Wildcards

Beyond digital threats, accommodation providers are bracing for disruptions they can't control. About 37 percent worry that extreme weather or natural disasters will tank bookings. Another 32 percent fret about local disruptions like transport strikes or infrastructure projects blocking access to their destinations.

These aren't theoretical anxieties. Border systems are getting more complex, flights are getting pricier, and climate volatility is real. Smart hoteliers now factor weather resilience and alternative access routes into their business plans as standard procedure.

The Seasonality Survival Game

To fight the feast-or-famine reality of tourism, 72 percent of European properties now run discounts and promotions during slow periods. Online platforms are the heavyweight champion of demand generation: 81 percent rely on them when occupancy dips. Social media and paid advertising come next, used by 54 and 50 percent respectively.

Event-driven tourism is emerging as a genuine business lever too. Half of properties report benefiting from events and special occasions, with two-thirds seeing stronger per-room revenue on those dates and 60 percent reporting higher bookings during traditionally slow periods. It's a reminder that travelers will venture out for the right reasons, even in shoulder seasons.

What This Means for Your Next Trip

For travelers, these shifts matter in concrete ways. Big chains mean consistency, modern amenities, and usually strong cybersecurity protecting your payment information. Independent properties offer character, local knowledge, and personalized service, but they're increasingly stretched thin competing for visibility and managing operational challenges.

The European accommodation sector is healing and growing, but it's doing so unevenly. If you want to stay somewhere special and support independent owners, now's the time to book directly and engage with smaller properties. They're more likely to remember you, more willing to accommodate quirky requests, and frankly, they need your business more than the megachains do.